The first thing you need to know is whether your job is covered by the Western Conference of Teamsters Pension Plan. This section explains the rules on Plan coverage and how your employer makes contributions based on your covered employment.

Important Topics

Covered Employment

Covered Employer

Union

Pension Agreement

Special Rules

Contribution Rate

Types of Contributions

Covered Hours

To participate in the Pension Plan, you don’t have to sign up or contribute. You simply work for a contributing employer who makes Plan contributions for your covered employment according to your collective bargaining agreement.

Covered Employment

Your work qualifies as covered employment only if your employer is a covered employer required to make contributions to the Pension Trust for your employment according to a written pension agreement.

Periods of employment for which contributions are not required do not count as covered employment, even if contributions are made for that employment. Not all work for a covered employer qualifies as covered employment. For example, your work does not qualify as covered employment if:

- You are not working in a job covered by a pension agreement.

- You are self-employed.

- You are a proprietor or partner of your business.

Covered Employer

A covered employer is any employer who is required to contribute to the Pension Trust by the terms of a pension agreement. Teamster local unions representing Plan participants can also cover their own employees by agreeing to make contributions to the Pension Trust.

An employer becomes a covered employer at the beginning of the first hour of covered employment performed by any employee. An employer stops being a covered employer at the end of the last hour of covered employment performed by any employee.

Union

Union means any local union affiliated with the International Brotherhood of Teamsters.

Pension Agreement

In general, to participate in the Pension Plan, you must be an employee covered under a pension agreement. In most cases, this is a written collective bargaining agreement (labor contract) between an employer and a Teamster local union that requires employer contributions to the Pension Trust on behalf of the employees who work under that agreement. The agreement must conform to Plan rules and policies and be accepted by the Board of Trustees.

Your pension agreement states what your employer’s basic contribution rate is and generally lists the job classifications that are covered by the Plan. It also tells you if your employer has agreed to make supplemental PEER contributions to the Pension Trust for your work (and the work of other employees covered by the pension agreement). If you need a copy, contact your employer or local union.

If you are an employee of a Teamster local union or joint council or other Teamster labor organization, your employer must sign a special pension agreement with the Board of Trustees to contribute to the Pension Trust. However, if your work for that employer is covered by a collective bargaining agreement with another labor organization, the pension agreement may exclude you from pension coverage under the Plan.

A local union outside the 13 Western states must meet special rules before it can contribute to the Pension Trust for its employees. Employees of other Teamster labor organizations (joint councils) outside the West cannot participate in the Plan.

Note: If you do not receive regular wages or salary compensation from the local union or joint council for your work as an employee, you are not eligible for pension coverage based on that work.

General Information

Only the Administrative Offices represent the Board of Trustees in administering the Plan and giving information about benefit amounts, eligibility and other provisions of the Plan. No representatives of any union, including union officers and business agents, no representatives of any employer or employer association, and no representatives of any other organization except the Administrative Offices, are authorized to provide information or interpret the Plan. In all cases, the Plan terms govern.

The Board of Trustees has the power to amend or terminate the Plan at any time. Click here to learn how a Plan amendment or termination can affect Plan benefits.

Self-employed persons such as sole proprietors, unincorporated owners and partners are not eligible to personally participate in the Plan.

Pensions are not paid to persons who are found to be ineligible for Plan coverage, even if contributions are made on their behalf. If you have questions about your eligibility for Plan coverage, write directly to your Administrative Office.

Special Participation Rules for Certain New or Reentering Groups

The Board of Trustees has established special rules that certain categories of employee groups must meet before the agreement they work under will be accepted as a pension agreement.

A local union representing one of these employee groups, or an employer of one of these groups, can review the Contribution Guidelines to learn about these special rules and what information the Pension Trust will require before deciding whether the employee group may join the Plan.

Here are the categories of employee groups that are subject to these special rules:

Employee Groups Subject to Special Rules

The following employee groups must satisfy special rules before they can become covered under the Plan:

- An employee group represented by a Teamster local union outside the 13 Western States.

- An employee group employed by a Teamster local union, joint council or other Teamster labor organization. Note: The only Teamster labor organizations outside the West whose employees can participate in the Plan are local unions.

- An employee group that was covered under the Plan at some time in the past, left the Plan and is now requesting to rejoin the Plan.

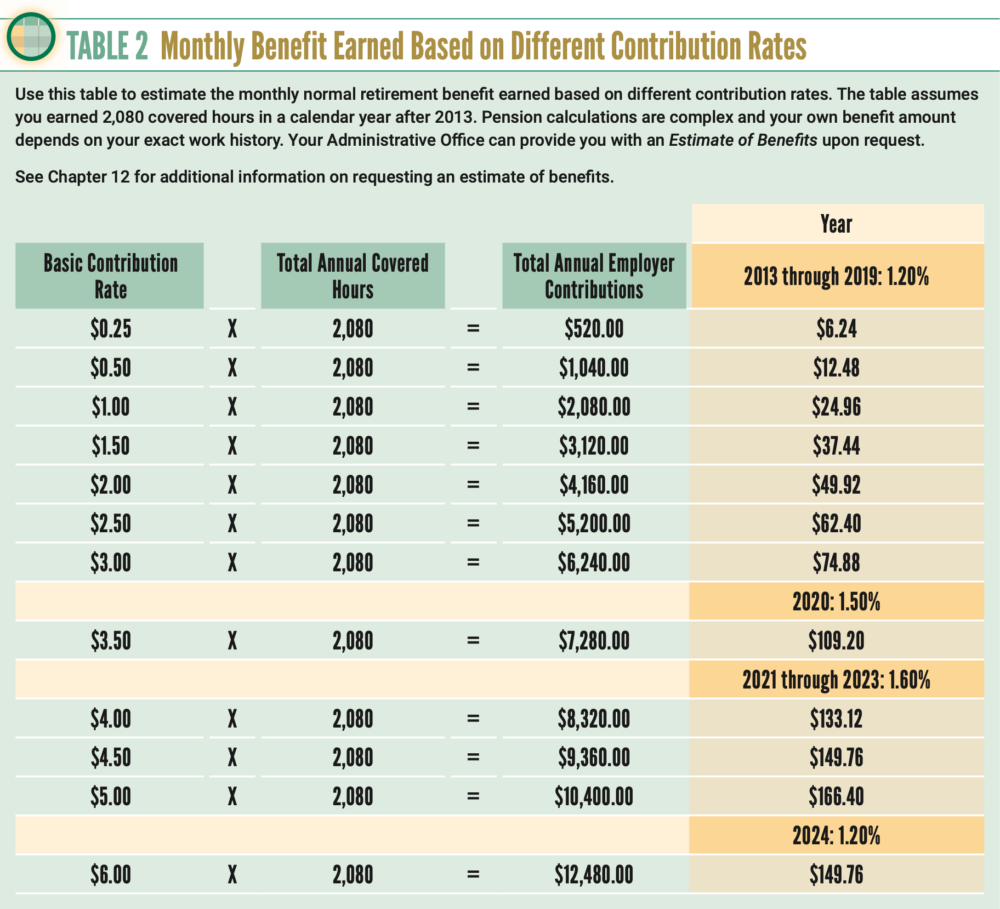

Contribution Rate

Your contribution rate is a set dollar amount that your covered employer is required to pay into the Pension Trust for your covered employment. It is based on a formula contained in your pension agreement and is determined through negotiations between your employer and your local union. Your contribution rate may be defined as an hourly, daily, weekly or monthly amount.

How much your employer contributes to the Pension Trust for your covered employment greatly affects the amount of your monthly benefit. Examples in Table 2 show how your benefit builds up faster as your contribution rate increases.

{kind=link}

Types of Contributions

There are two types of contributions that covered employers make to the Pension Trust: Basic contributions and PEER contributions. You need to understand the difference because only basic contributions are used to calculate the amount of your Plan benefit.

Basic Contributions

Basic contributions are a major part of the total contributions that covered employers pay into the Pension Trust for your covered employment. They are used to help pay for the basic benefits your Plan provides. The exact contribution rates for your work are specified in your collective bargaining agreement.

PEER Contributions

First introduced in 1992, the Program for Enhanced Early Retirement (PEER) lets eligible participants retire early at any age with no reduction in benefit amounts. Most of your Plan’s employers make separate PEER contributions to help pay for enhanced early retirement benefits through PEER.

PEER contributions are paid in addition to the basic contributions your employer is required to make. They are not used to calculate the amount of your Plan benefit. Your pension agreement tells if your employer makes PEER contributions. Click here for information about PEER.

Belonging to a union or paying union dues does not necessarily mean you have Plan coverage. Contact your Administrative Office if you have questions about your coverage.

Belonging to a union or paying union dues does not necessarily mean you have Plan coverage. Contact your Administrative Office if you have questions about your coverage.

Covered Hours

Covered hours are important. Unlike other types of hours of service, which only count toward vesting, covered hours also count toward:

- Maintaining your recent coverage, which is a key eligibility requirement for many Plan benefits.

- Determining the amount of your Plan benefits.

- Qualifying for higher early retirement benefits under the Rule of 84.

- Qualifying for unreduced early retirement benefits if you are covered by a PEER pension agreement.

A covered hour is an hour of your employment for which your employer is required to make contributions to the Pension Trust under the terms of a written pension agreement. Hours of work (or paid time off) for which no employer contributions are required by your pension agreement do not count as covered hours.

Many Plan requirements depend on the number of covered hours you have in a specific time period (such as the calendar year). It’s important to know which of your hours of employment are covered hours.

Although many pension agreements require contributions for all paid hours, some agreements only require contributions on straight time hours with no contributions for overtime hours.

Other agreements contain daily, weekly, monthly or yearly maximums that limit the number of hours for which contributions are payable. Hours worked beyond those limits do not count as covered hours.

Some agreements require contributions for certain paid time off such as holidays, vacation, jury duty or sick leave while others do not.

Check the specific language of your collective bargaining agreement for details about the kinds of hours that require employer contributions.

What Hours Require Pension Contributions?

Your covered employer is required to pay pension contributions to the Pension Trust on your behalf based on the specific provisions of your pension agreement. Your employer may not be required to contribute to the Pension Trust for every compensable hour. Under Plan rules, every pension agreement must provide for contributions for all straight time hours, including vacation and sick time, subject to certain permissible limitations that must be set forth in the pension agreement.

Most contracts have monthly or yearly maximums on employer contributions. Some contracts exclude specific compensated hours such as overtime. Here are examples of the most common limitations in pension agreements about required pension contributions.

Monthly Maximums

If your pension agreement contains a monthly maximum, then your employer is not required to contribute for any compensable hours you earn over the maximum number of hours in a calendar or reporting month. The most common monthly maximum is 184 hours.

Yearly Maximums

If your pension agreement contains a yearly maximum, then your employer is not required to contribute for any compensable hours you earn over the maximum number of hours in a calendar year. The most common yearly maximums are 2,076 and 2,080 hours. Lower maximums are not permitted under Plan rules.